Sugar imports are expected to decline by 30% in MY 2024/25 to 455,000 MT, as domestic production surges.

Kenya’s sugar imports more than doubled in January 2025, driven by a sharp increase in industrial sugar demand.

The East African region consumes approximately 1.5 million MT of sugar annually, presenting significant export opportunities for high-quality sugar producers

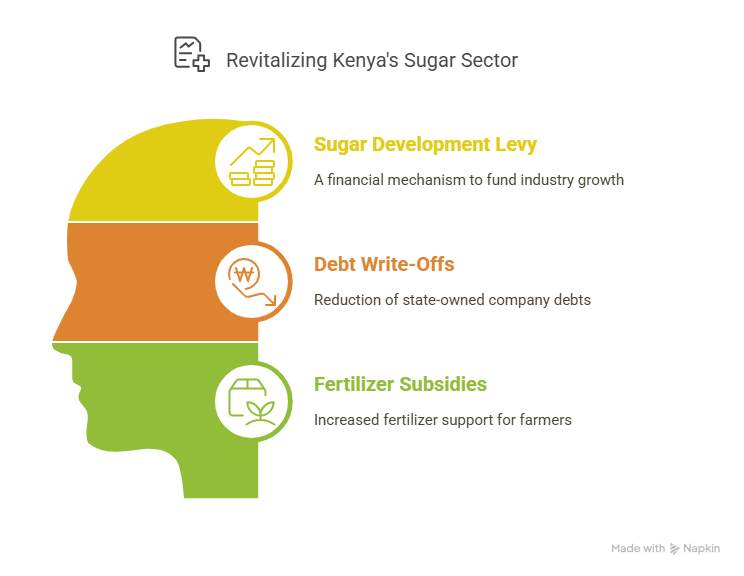

The Sugar Act of 2024 introduces a Sugar Development Levy to fund industry growth and support farmers.

The government has written off Sh67 billion in debts owed by state-owned sugar companies and increased subsidized fertilizer allocations to 1 million bags in 2024, up from 700,000 bags in 2023.

A sugarcane pricing committee has been established to ensure equitable returns for growers and millers, with the minimum sugarcane price rising to Ksh 5,300 per tonne in February 2025

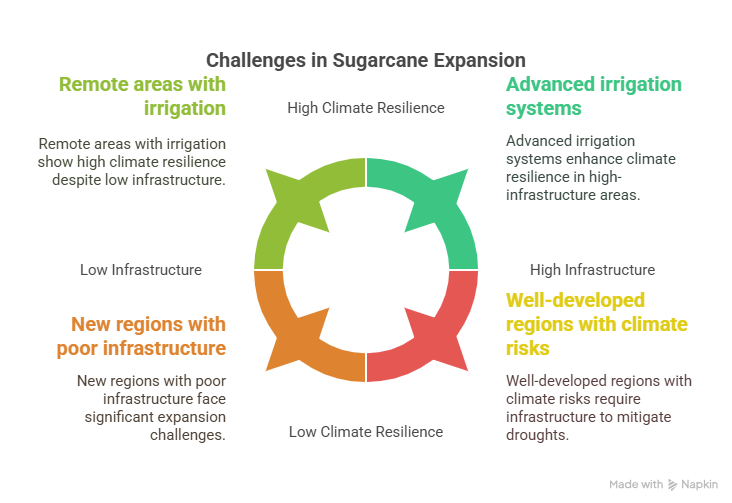

The government is exploring new sugarcane-growing frontiers, including the Tana River Delta, Bura Irrigation Scheme, and Kerio Valley, to diversify production beyond traditional areas in Western Kenya.

These regions offer fertile soil and irrigation potential, making them ideal for large-scale sugarcane cultivation

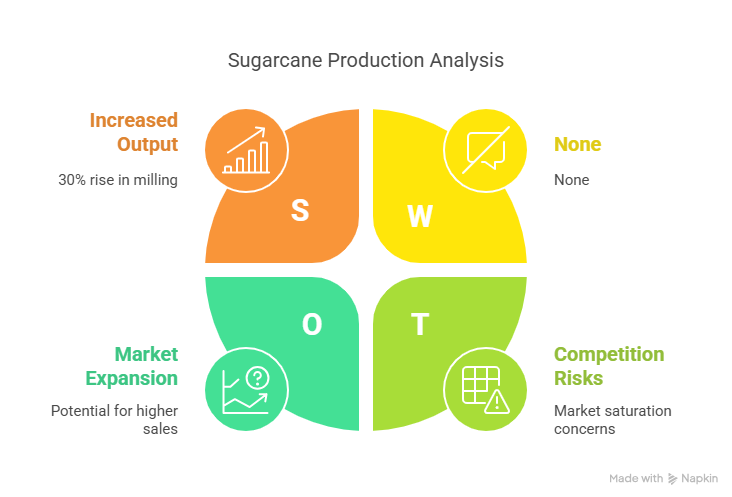

Sugarcane milling increased by 30% to 827,482 MT in January 2025, with sugar production rising by 22% to 73,019 MT

The cane-to-sugar ratio (TC/TS) improved to 10.64 in February 2025, up from 11.33 in January, reflecting enhanced processing efficiency

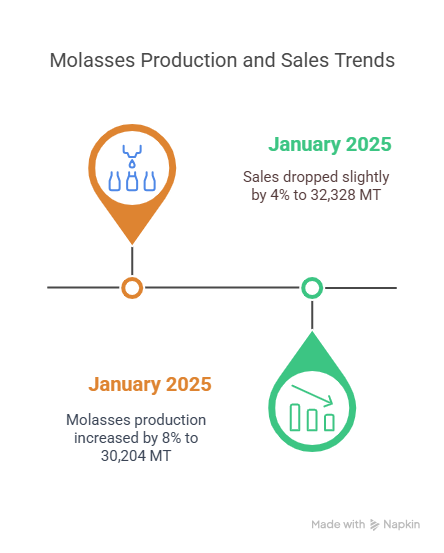

Molasses production increased by 8% to 30,204 MT in January 2025, with sales dropping slightly by 4% to 32,328 MT

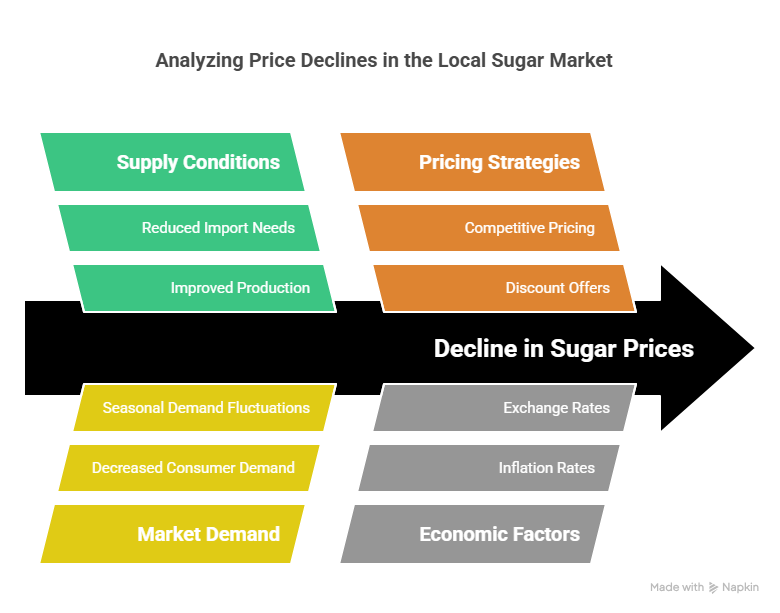

The ex-factory price of sugar decreased by 0.7% to Ksh 6,525 per 50kg bag in February 2025, while the retail price averaged Ksh 156 per kilo.

The wholesale price declined by 6% to Ksh 6,712 per 50kg bag, reflecting improved supply conditions

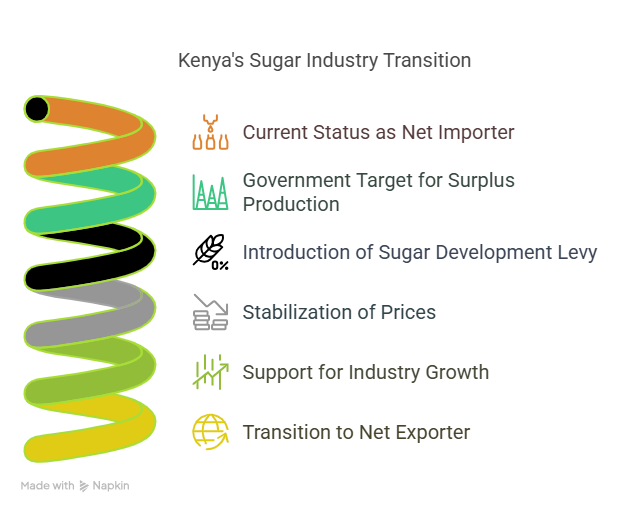

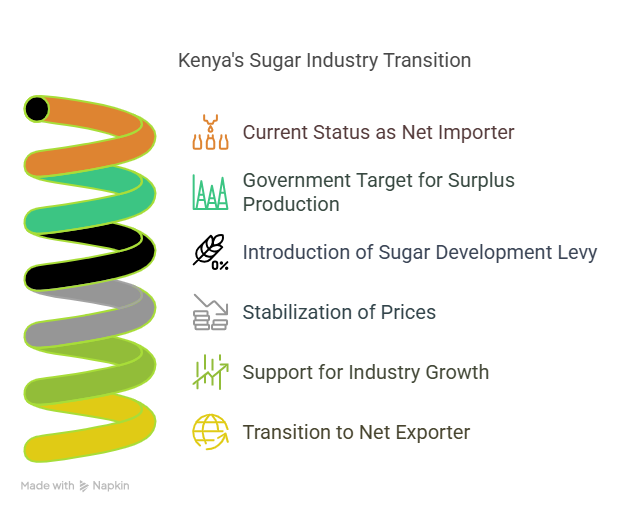

Kenya’s sugar industry is poised to transition from a net importer to a net exporter, with the government targeting surplus production by 2027.

The introduction of a Sugar Development Levy on both domestic and imported sugar aims to stabilize prices and support industry growt

Infrastructure limitations in new sugarcane-growing regions pose challenges to expansion efforts.

Droughts and climate variability remain risks, though irrigation systems are mitigating these impacts

The high sucrose content and rapid growth cycles of sugarcane in the Tana River Delta offer premium-quality production and higher yields.

Cogeneration and ethanol production from sugarcane by-products present additional revenue streams, enhancing the sector’s profitability